In March 2019, Singapore was announced the most expensive city in the world to live in (alongside Paris and Hong Kong). Yet property is still an asset people will invest in because of the potential it possess.

If you’re investing in your 2nd (or subsequent) property, here are 7 things to know about Additional Buyer Stamp Duty (ABSD): who is liable to pay it, the exemptions, how to beat the tax, and so on.

Also read: 2 Key things to look out for when you get your 2nd home loan

The Additional Buyer Stamp Duty (ABSD) applies to owners who purchase their second and subsequent property. It’s an extra tax the government imposes on residential properties (e.g., condominiums, private estates, HDB flats, shophouses with live-in residences, etc.)

ABSD acts as a cooling measure to curtail the booming property market. Given that real estate prices skyrocketed by 9.1% in 2018, the Singapore government needed to put in place something that would prevent housing prices from going up further.

If the increased demand had been left unchecked, the upward trend would have led to a housing bubble. In such a bubble, many are likely to commit to loans they cannot afford, which increases the risk of foreclosures. When the bubble bursts, it would’ve led to more foreclosures, an oversupply of houses, and low demand

You have to pay ABSD if you are a…

That’s right: for PRs and foreigners, even if this is your first property purchased in Singapore, you are liable to pay for ABSD.

As long as you own a shared interest in a property (even if that’s an investment property with your siblings), you are liable to pay for ABSD. Any other property purchased will be considered as your 2nd property. If paying the ABSD is an issue, you may want to rethink keeping your stake in the shared property.

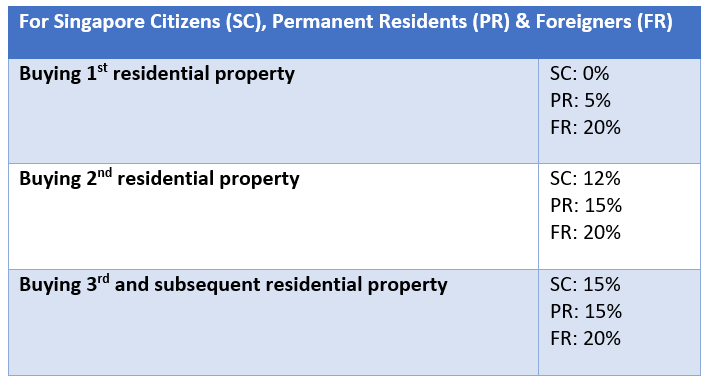

With the new regulations in play, homeowners can expect a 12% or higher ABSD rate on the current valuation of the property or the selling price, whichever is higher.

The current ABSD rates are as follows:

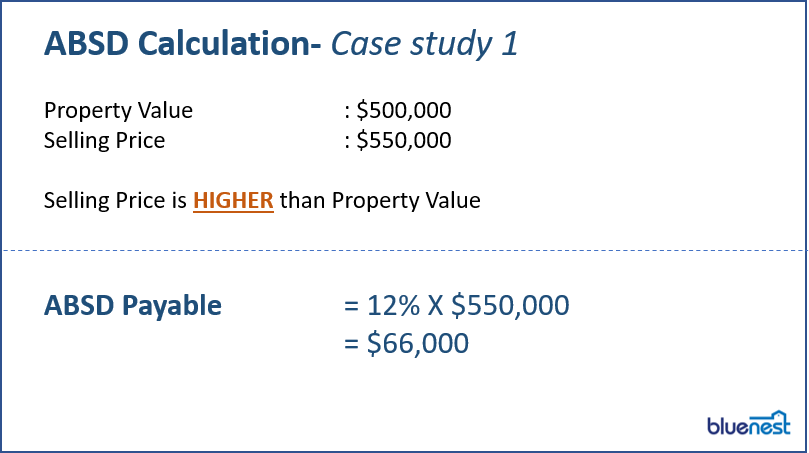

Case Study 1:

Sam is a Singaporean citizen looking to purchase his 2nd residential property for investment purposes. The property is valued at $500,000. He agrees to buy it at $550,000.

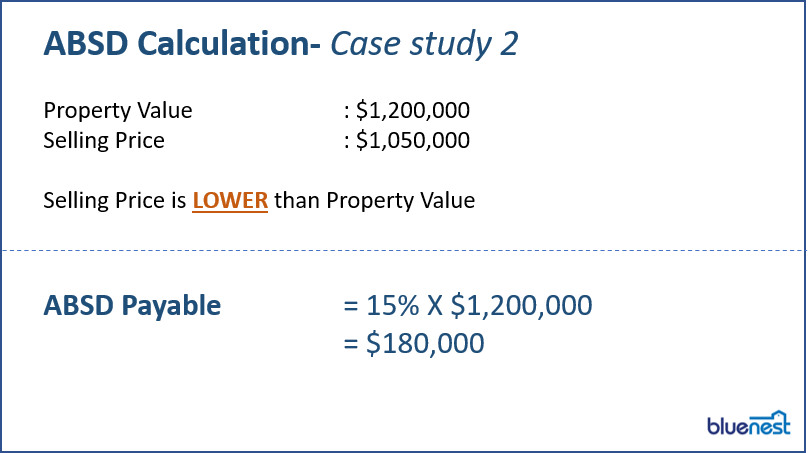

Case Study 2:

Martha is a Malaysian PR looking to purchase her 2nd condominium to rent out. The property is valued at $1,200,000. After negotiations, she purchases it at $1,050,000.

ABSD can be paid via NETS, cheque, or cash order through the e-Stamping Portal. Other avenues include IRAS e-terminals or specific branches of SingPost Bureaus (Shenton Way, Novena, Chinatown, and Raffles Place).

While CPF (Ordinary Account) funds can be used to pay your ABSD, you have to pay out of your pocket first before getting reimbursed from your CPF account.

The deadline to pay is within 14 days for contracts signed in Singapore, and 30 days for contracts signed overseas. You’ll want to pay punctually to prevent paying the hefty penalty (which can be 4 times your ABSD!).

You won’t have to pay the ABSD if:

ABSD can eat into your finances. One of the most common ways to avoid the tax is decoupling – essentially, transferring your share of the property to your spouse. Afterwards, you’ll be free to purchase your 2nd property as though it’s your first.

Your spouse will have to pay the Buyer Stamp Duty and all the associated legal fees when they take over your share, but this is generally far cheaper than the ABSD. (Read also: Can I Transfer My Share of the House to My Spouse/Child to Avoid ABSD?)

Was this article helpful? Good things must share!